Last updated: 8 April 2026

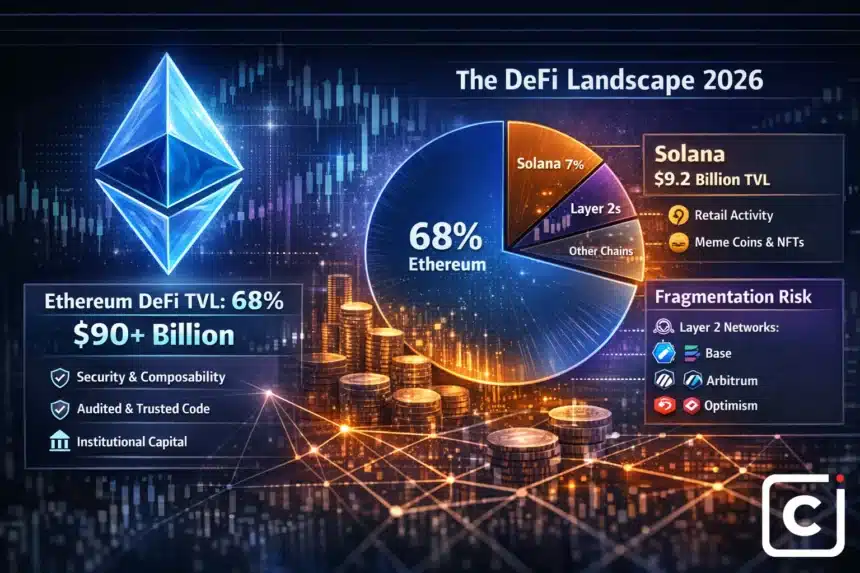

Total DeFi TVL across all blockchains sits at approximately $130 to $140 billion in Q1 2026. Ethereum accounts for 68% of it. Solana, which has won the narrative battle for retail attention over the past 18 months, holds roughly $9.2 billion, less than 7%. Every Layer 2 network, every alternative Layer 1, and every modular chain combined does not add up to what Ethereum holds alone. The question is no longer whether competitors can overtake Ethereum. The question is why they have not, and whether anything changes in the next two years.

Key Highlights

- Ethereum DeFi TVL: approximately 68% of $130 to $140 billion total in Q1 2026

- Solana DeFi TVL: approximately $9.2 billion, roughly 7% of total

- All Ethereum Layer 2 networks combined: growing but still subordinate to Ethereum mainnet settlement

- Ethereum post Pectra: validator cap raised to 2,048 ETH, blob throughput doubled

- Smart contract composability, audited code, and institutional trust drive stickiness

- Key risk: Layer 2 fragmentation is splintering Ethereum’s own liquidity internally

Why TVL Is the Right Metric Here

DeFi TVL measures capital that is actively deployed in smart contracts: lending protocols, liquidity pools, staking vaults, and derivatives. It is not price. It is not trading volume. It is money that users and institutions have chosen to trust to code on a specific chain.

When Ethereum holds 68% of that number, it means that the overwhelming majority of the world’s capital deployed on chain is sitting in Ethereum smart contracts. That is a trust signal. Large capital holders, whether they are market makers, institutions, or sophisticated retail, have chosen Ethereum as the place where they are willing to lock up real money.

Trading volume and daily active users are where Solana wins, particularly for activity driven by retail. But TVL is the institutional proxy. And on that metric, Ethereum’s lead has not narrowed materially since 2021.

The Structural Reasons Ethereum Holds Its Position

The most commonly cited reason is security. Ethereum’s validator set is the largest and most decentralized of any smart contract platform. For institutional DeFi participants, particularly those managing billions in assets on chain, the cost of a security failure far outweighs any gas fee savings from migrating to a faster chain.

The second reason is composability. Ethereum’s DeFi ecosystem was built over years with protocols designed to work together. Aave, Uniswap, Maker, and Compound interact in ways that create compound yield strategies unavailable on any other chain. Replicating that ecosystem elsewhere requires not just copying the protocols but rebuilding the network of trust and integration that makes them composable. No competitor has done that.

The third reason is audited code. The most critical DeFi infrastructure on Ethereum has been audited dozens of times by every major security firm, proven through years of use with billions in on chain activity, and iterated over time. Newer chains offer speed and lower fees but ask capital holders to trust contracts with months of history, not years. For large capital, that is not a trade off most are willing to make.

What Solana’s $9.2 Billion Actually Means

Solana’s $9.2 billion in DeFi TVL is not a failure. It is one of the largest DeFi ecosystems ever built on a chain outside Ethereum. Solana’s success in capturing retail trading volume, meme coin activity, and NFT markets is real and documented.

But Solana’s TVL is concentrated in a small number of protocols such as Marinade, Jupiter, and Orca, and is heavily weighted toward liquid staking and DEX liquidity rather than the diversified DeFi stack that characterizes Ethereum. For Solana to meaningfully challenge Ethereum’s TVL dominance, it would need institutional capital to deploy at scale in lending and derivatives protocols. That has not happened yet.

The Real Threat: Ethereum Fragmenting Itself

The most credible challenge to Ethereum’s DeFi dominance is not Solana or any external competitor. It is Ethereum’s own Layer 2 ecosystem. Base, Arbitrum, and Optimism collectively host billions in TVL, but that TVL exists on separate execution environments. Liquidity on Base cannot directly interact with liquidity on Arbitrum without bridging, which adds cost, latency, and security risk.

As Layer 2 activity grows, it does not consolidate back onto Ethereum mainnet. It stays on Layer 2. The question for 2026 and 2027 is whether interoperability between Layer 2 networks improves fast enough to prevent capital from scattering across incompatible environments, reducing the composability advantage that makes Ethereum DeFi valuable in the first place.

The TCB View

Ethereum’s 68% DeFi TVL share in 2026 is not a sign of stagnation. It is a sign of how difficult it is to displace infrastructure that institutional capital trusts at scale. The competitors that matter are not Solana or Avalanche. They are Base and Arbitrum, networks that inherit Ethereum’s security while capturing activity that used to stay on mainnet. The internal fragmentation risk is more interesting than any external competition right now. Watch how the Ethereum Foundation approaches Layer 2 interoperability in the next two upgrades. That is where the real battle is being fought.

Free Daily Briefing

Get the Daily Briefing

Crypto, AI, and Web3 intelligence. Free, every day.

The Daily Brief by TCB

Crypto, AI & finance intelligence in 5 minutes. Every weekday morning. Free.