The L2 narrative of 2023 and 2024 was simple: Ethereum needs to scale, rollups are the answer, and more rollups means more choice. Today, in March 2026, we can audit that thesis against reality.

The result is uncomfortable for most of the teams that shipped chains.

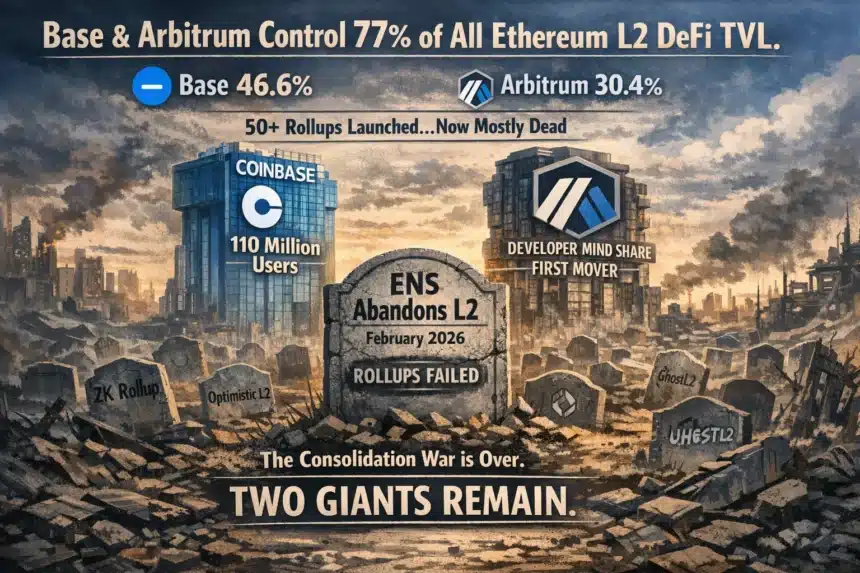

Base and Arbitrum control 77% of all Ethereum L2 DeFi TVL. Base alone sits at 46.6%. Approximately 50 other rollups divide the remaining 16.5% and most of them are functionally inactive.

Key Highlights

- Base holds 46.6% of all L2 DeFi TVL and over 1 million daily active addresses, making it the dominant Ethereum layer 2 by every meaningful metric

- Arbitrum holds 30.9% and remains the clear second, with incremental upgrades rather than dramatic shifts

- Approximately 50 other rollups split 16.5% of TVL, with most functionally inactive after incentive programs ended

- ENS scrapped its planned L2 rollout in February 2026, citing fragmentation costs — a clear signal from an established protocol

- Base won through Coinbase’s 110 million user distribution, not technical superiority — the stack is identical to Optimism’s

- The consolidation war is over. Build where the users are

The Numbers That Tell the Story

Base: 46.6% of L2 DeFi TVL. Over 1 million daily active addresses. Consistently capturing around half of all DEX volume across the entire L2 ecosystem.

Arbitrum: 30.9%. TVL largely stable year-over-year, still the clear second. The ArbOS Dia Upgrade in January 2026 improved gas fee predictability and added Passkey authentication.

Optimism: approximately 6%. OP Mainnet benefited from Superchain expansion but lost retail attention almost entirely to Base. That is notable given Base runs on the OP Stack and Optimism collects protocol fees from that growth.

Everyone else: 16.5% split among roughly 50 chains, most of which saw activity collapse after their incentive cycles ended.

Why Base Won

Base is built on the OP Stack. So is Optimism. So are dozens of other chains. The stack is open source, freely available, and technically equivalent. Base did not win because it solved a hard engineering problem.

Base won because Coinbase has 110 million verified users. When Coinbase Wallet defaults to Base, when Coinbase Commerce settles on Base, when 110 million retail accounts get a prompt to use Base for lower fees, the flywheel spins faster than any liquidity mining program ever could.

Arbitrum won its position through developer mindshare and the advantage of moving first in the DeFi summer era. Base won through retail distribution. Both are moats. Neither is replicable by a team that launches a chain without an existing user base.

How 50 Chains Died the Same Death

The playbook that killed most L2s ran on a precise schedule: launch chain, announce liquidity incentives, watch TVL spike as mercenary capital pours in, hold a token generation event, end incentives or unlock tokens, watch liquidity migrate to Base or Arbitrum, become a ghost town.

The variation between chains was cosmetic. The outcome was nearly universal. The fundamental error was assuming that TVL during an incentive period reflected genuine user demand, and that users would stay once the incentives stopped. They did not. They never do.

ENS’s Retreat: The Clearest Signal Yet

In February 2026, Ethereum Name Service scrapped its planned Layer 2 rollout. ENS cited Vitalik Buterin’s comments on the complexity and fragmentation costs of separate chains, and concluded that launching a rollup no longer justified the marginal scaling benefit for their use case.

ENS is one of the most established, genuinely used protocols in the Ethereum ecosystem. It has real users, real revenue, and real technical depth. If ENS cannot justify its own rollup, it is a serious signal about the viability of standalone L2s for all but the largest teams with existing distribution advantages.

What This Means for Builders

The map is settled. Base and Arbitrum own the terrain. This is not a temporary state. It reflects structural advantages in distribution, liquidity depth, developer tooling, and brand recognition that compound over time.

Build on Base if you are building consumer products or need access to Coinbase’s onboarding funnel. Build on Arbitrum if you are building DeFi infrastructure or institutional products that need the deepest liquidity. Build on mainnet if your use case genuinely requires L1 security guarantees and you can absorb the gas costs. Do not build your own L2 unless you have the distribution to fill it.

Glamsterdam’s L1 scaling improvements will raise the throughput floor for all surviving rollups, which could shift the economics of the consolidation further.

Builders choosing which chain to deploy on are also watching the regulatory classification of crypto assets, which now shapes which tokens L2 protocols can safely support.

The TCB View

The market did not fail. The narrative failed. L2 consolidation was always the likely outcome once distribution mattered more than technical parity. Base and Arbitrum did not win by being better rollups. They won by being better businesses.

That is the lesson builders should carry forward. In a multi-chain world, user acquisition compounds just like DeFi yields do. The protocol that starts with 110 million users does not need a better stack. It needs to not break anything. Coinbase did not break anything.

ENS’s retreat is the punctuation mark on this era. When a protocol with real users and real revenue decides that launching its own chain is not worth it, the question every other team should ask is: what do we have that ENS does not? In most cases, the honest answer is nothing.